When applying for an auto loan from a lender (like a bank, credit union, or even a dealership) you're likely to hear about interest.

When applying for an auto loan from a lender (like a bank, credit union, or even a dealership) you're likely to hear about interest.

Interest on an auto loan is essentially the extra fee you pay for using the lender's money to buy a car. Luckily, the interest you'll accrue (and eventually owe) on your loan is spread out over the life of your loan, so you're not required to pay the fee back all at once.

QUICK TIP: You can lower the amount of interest you pay on your loan by paying more than the minimum required monthly loan payment each month. Or avoid interest altogether when repaying the lender in full (if possible). |

Some common questions we're asked at the credit union include:

-

- How do lenders determine which interest rate to offer?

- Will my interest rate change over time?

- How is my interest rate calculated?

- What's considered a good interest rate on an auto loan?

These are all valid and excellent questions you should ask a lender before applying for an auto loan!

but... here's the frustrating part:

Unfortunately, you won't know your actual interest rate until you're either approved or pre-approved for the loan. In addition, if you're approved for the auto loan, but you're not quite ready to move forward, you could lose that interest rate and auto loan offer after a certain period of time (typically, pre-approvals are good for 30 days).

QUICK TIP: If you're unsure about an auto loan but want an idea of how much money you could be approved for, simply pre-qualify! I talk more about this in The Pros and Cons of Getting Pre-Qualified for an Auto Loan. |

In this article, I'll offer some peace of mind and share some factors lenders consider when determining your interest rate so you're better prepared.

here's what we'll cover:

|

|

how do lenders determine what interest rate to offer on an auto loan?

how do lenders determine what interest rate to offer on an auto loan?

The interest rate you receive on an auto loan is based on a few factors, including:

- Credit Score & History: When lenders review your credit score and history, it tells them how many lines of credit you have or if there are negative marks on your credit report. If you have a good credit score (above 700), you can expect to receive a lower interest rate. Your credit score is not the only factor that determines your interest rate, but it's certainly the most important!

QUICK TIP: Request your free credit report every 12-months, so you'll have a good idea of what your score is before walking into the dealership or financial institution. Get your credit report for free at annualcreditreport.com. |

- The Amount You're Requesting To Borrow: Lenders also look at your previous auto loan amounts and payment history to ensure you can handle the loan. A large down payment on an auto loan reduces how much you’ll owe, helps to secure the loan amount, and tells the lender you're serious about paying it back.

- Debt-to-Income Ratio (DTI): Lenders determine your borrowing risk based on the percentage of your gross monthly income that pays your monthly debt payments. So, if you have a debt ratio above 50%, you'll have more difficulty finding a reputable lender to finance your loan.

- The Loan Term (aka the Life of the Loan): A short loan term could mean larger monthly payments (but less interest paid over the life of the loan) while longer loan terms typically mean lower monthly payments (but more interest paid over the life of the loan). 36- to 72-months is the average loan term.

- The Vehicle You're Financing: Typically, the older your car is, the higher your interest rate will be simply because it has a lower value.

what’s considered a good interest rate?

what’s considered a good interest rate?

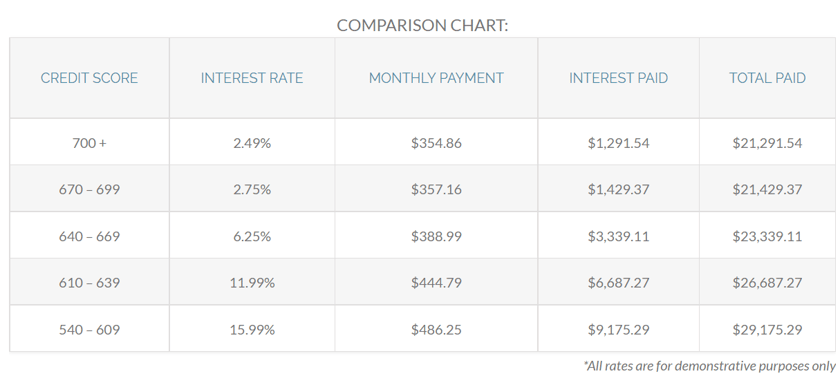

Interest rates vary based on the lender, but you can generally expect a lower interest rate when borrowing from a credit union or a bank compared to the dealership. Credit unions specifically offer lower interest rates to their members simply because they're not focused on making profits (Psst... credit unions have better approval odds for a loan due to bad or no credit at all. Here’s why.).

|

The comparison chart below is for demonstrative purposes only, but it can help you gain a better understanding of how interest rates are calculated. It includes a range of credit scores to help you better understand how lenders reach their calculations on interest rates.

how is my interest rate calculated?

how is my interest rate calculated?

Want to calculate your interest rate? Here's what you'll need:

- An Excel Spreadsheet: This is where you’ll calculate loan details using the formula provided below. Google Sheets are also available on mobile devices. You can download it for free in the Play Store or the App Store.

- The Desired Loan Amount: This is the amount you're looking to finance.

- Loan Term: The length (usually listed in months) of your auto loan.

- The Loan’s Interest Rate: This can be a rate that was offered by your lender, or you can use any of our interest rates on our website (check out our current rate list for available rates). Since the interest rate on a loan is typically noted on an annual basis, we'll be calculating the Annual Percentage Rate (APR).

- Additional Fees: This could include an origination fee (a fee charged by the lender), GAP insurance, title transfer fee, fees for new tags, or property / highway tax. Also, consider dealer fees which could include a wide range of charges if you're financing through the dealership.

Feel free to use the credit scores on the comparison chart above to help you get a sense of the interest rate you could receive when borrowing from a lender and calculating your estimated APR.

QUICK TIP: Change your cell format before you start calculating! When calculating the monthly payment using Google Sheets or Excel, make sure your cell number format is changed to Accounting. When calculating the interest rate using Google Sheets or Excel, make sure your cell number format is changed to Percent. |

ready to start calculating?

Let’s say:

-

- You’re looking to finance a vehicle for $15,000 ($14,500, plus $500 in fees)

- Your loan term is 72 months

- You have an interest rate of 8.99% APR

how To determine your monthly payment:

On your spreadsheet (i.e. Google Sheet or Excel), use the following formula to begin calculating your monthly payment:

|

how to calculate your estimated interest rate:

On your spreadsheet (i.e., Google Sheet or Excel), you’ll use the following formula to help you calculate your estimated interest rate:

|

If you're not a fan of spreadsheets, there are plenty of interest rate calculators online you can check out instead. Calculator.net includes a detailed breakdown of terms as well as a chart and graph showing the principal and interest breakdown.

You can also use Skyla's loan payment calculator to find your monthly payments, total interest, and total loan cost. It helps to know your loan information, such as the loan amount, loan term (months), interest rate, and payment frequency.

quick tip - the amount you pay in interest each month will differ. here's why....

Auto loans are typically offered at a fixed interest rate, meaning the interest rate doesn't change but the amount you pay for interest might. Interest on auto loans is calculated daily based on your total loan balance and depending on your payment habits, you could be paying more or less in interest each month on your auto loan.

Let’s break it down - Say you received a $10,000 auto loan with a 13.740% APR. You have 60 months (5 years) to repay that loan amount on top of the interest that's calculated daily. If you break that down month to month, your monthly payment would roughly be $231.

The $231 is made up of the interest amount and the principal amount (the amount that's going towards paying down that initial $10,000 loan). Here's an amortization chart so you can see the basic breakdown of the monthly payment for the first 6 months.

* The figures in this table are for demonstrative purposes only.

what if I'm late making a payment?

If you were late making your monthly payment, expect that payment to go towards penalty fees first. Afterward, the rest of the payment would go towards the increased interest amount because you're more than 30 days late on your auto loan. Keep in mind, being late on your auto loan payment could open the door to paying more money like an increase to your overall borrowing cost.

The best way to avoid paying more interest or avoid interest accruing on your auto loan, make sure you:

- Pay your auto loan on time or in advance of the due date.

- Pay the amount due or pay more than the minimum amount each month.

here's what’s next:

here's what’s next:

Remember... interest will (most likely) be involved when financing a vehicle. Feel free to use the options above (interest rate formula, Skyla's calculators, or visit Calculator.net ) to calculate your interest. And don't forget to grab your free credit reports from annualcreditreport.com once every 12 months!

QUICK TIPS: |

Now that you understand what goes into calculating interest on an auto loan, you'll be more confident talking to your preferred lender when discussing rates.

calculate your interest

calculate your interest

Here's how lenders determine your interest rate, the formula used to calculate the interest rate, and more...

learn auto refi

learn auto refi

Want to lower your auto loan payments? Refinancing could reduce your rates and save you money.

know when to refinance your auto

know when to refinance your auto

Here's when to refinance your auto loan. It could be the perfect moment to save money and put cash back in your pocket!